Octane Capital is a UK-based specialist lender founded in 2017, providing a range of banking products and services to SMEs, property professionals and consumers, including bridging loans.

Since launch, they have lent over £1.5 billion across more than two thousand different loans, focusing on complex cases and profiles.

In this review, I will take a closer look at Octane, detailing their products’ key features, eligibility criteria, application process, rates and reviews to help you decide whether they are the right option for your bridging financing needs.

Octane Bridging

Octane offers a range of bridging loans from £200,000 to £25,000,000 for both residential and semi-commercial needs.

These loans can be used to quickly secure property purchases, fund refurbishments, raise capital, or refinance existing loans.

Key features include

- Bridging loans from £200,000 up to £25,000,000, with up to 70% LTV available

- Rates start from 0.36% (+BBR) per month for terms up to 18 months

- Flexible on borrower profile

- Flexible on interest payment methods

- First-time buyers accepted

- Rates are indexed on the Bank of England’s

- Quick completion process

- Same-day credit backed terms

- Experience is not always required for refurbishment loans

- No exit penalties

Overall, Octane has an excellent reputation. The application process is simple, the team is helpful, and a good number of cases are accepted, even when borrowers have a complex credit profile.

What are the Eligibility Criteria for an Octane Bridging Loan?

Bridging Criteria

| Criteria | Value |

|---|---|

| Amount | £200,000 to £25,000,000 |

| Residential LTV | Max. 70% |

| Commercial LTV | Max. 65% |

| Term | Up to 18 Months |

| Interest Repayment | Rolled-up, Serviced or Retained |

| Exit Penalties | ❎ |

| Accepted Securities | All types of residential property / Semi-commercial property / Commercial property / MUFBs / HMOs / Student lets |

| Adverse Credit | ✅ |

Buy-to-Let Criteria

| Criteria | Value |

|---|---|

| Amount | £150,000 to £25,000,000 |

| Max. LTV | 75% |

| Term | Up to 5 years |

| Interest Repayment | Rolled-up, Serviced or Retained |

| Accepted Securities | All types of residential property / Semi-commercial property / MUFBs / HMOs / Student lets |

| Adverse Credit | ✅ |

Refurbishment Criteria

| Criteria | Value |

|---|---|

| Amount | £200,000 to £25,000,000 |

| Max. LTV | 75% |

| Max. GDV | 70% |

| Interest Repayment | Rolled-up, Serviced or Retained |

| Accepted Securities | All types of residential securities / Semi-commercial properties / MUFBss / HMOs / Student lets / Offices with permitted development / Commercial assets with residential planning permission |

Developer Exit Criteria

| Criteria | Value |

|---|---|

| Amount | £150,000 to £25,000,000 |

| Max. LTV | 75% |

| Term | Up to 18 Months |

| Interest Repayment | Rolled |

| Accepted Securities | Multi-unit residential schemes / Semi-commercial schemes / Completed permitted development schemes / No max unit value / Will take commercial views on availability of warranties / Pre or post marketing launch |

Application Process for Octane Bridging

The application process for an Octane bridging loan is extremely simple. It all starts with filling out an enquiry form.

Enquiry – Send the filled-out form to Octane by email or fill it out directly from the website.

AIP – The broker completes the form. Your signature is not required at this point.

Offer – If you meet the loan’s requirement, Octane will issue credit-back terms within a day, instruct solicitors, and start the valuation process.

Legal – Octane’s solicitors will issue the formal loan offer.

Completion – The funds are released, and the procuration and broker fees are paid on the same day.

The front-end process is quick and straightforward, with minimal information needed upfront. More due diligence comes before formal approval.

Octane Rates

| Loan Type | Rates From | Max. LTV | Apply |

|---|---|---|---|

| Bridging Loan | 0.36% pcm + BBR | 70% | More Info |

| Buy-to-Let Loan | Variable | 75% | More Info |

| Refurbishment | 0.38% PCM + BBR | 70% | More Info |

| Developer Exit | 0.36% PCM + BBR | 70% | More Info |

Fees

| Fee | Description | Value |

|---|---|---|

| Valuation Fee | Used to calculate how much we will lend you | Variable based on 3rd party cost |

| Legal Fee | Legal fees and costs as part of the sollicitors’ work on behalf of the lender | Variable based on 3rd party cost |

| Re-Inspection Admin. Fee | Charged if your loan has a works facility | £295 |

| Unpaid Direct Debit | Payable when your nominated bank rejects a direct debit collection | £20 |

| Property Related Cost | This fee covers the cost of contacting you for non-payment of property related costs | £145 |

You can find the full list of Octane fees here.

Octane Reviews & Ratings

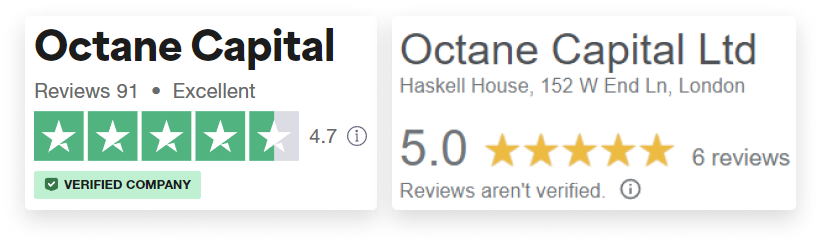

Overall, Octane Capital receives very positive reviews, earning an ‘Excellent’ TrustScore of 4.7 out of 5 based on over 90 reviews on Trustpilot and 5 our of 5 on Google Reviews, based on 6 reviews.

The majority of reviews rate Octane 5 stars. Customers praise the easy application process, and fantastic customer service. Many note getting loan approval within 24 hours.

The negative reviews mainly relate to case denials and delays, but they are limited compared to the overwhelming positive feedback.

In summary, reviews indicate high customer satisfaction with Octane’s lending services, owing to fast processing, flexible terms, and helpful staff. While a minority of customers have faced challenges, my overall sentiment toward Octane is very favourable.

Compare bridging loans

Save time and money with Business Expert & Fluent Bridging

Quick Search – Compare bridging loan criteria in real time

Easy Process – Answer a few quick questions about your loan needs

Expert Support – Get access to our partner’s in-house advisers

Octane Capital FAQs

What Types of Properties Are Eligible for Octane Capital’s Bridging Loans?

Octane Capital provides bridging loans for all types of residential and semi-commercial properties.

Who Can Apply for Octane Capital’s Bridging Loans?

Octane Capital is flexible on borrower profiles and can lend to various entities including foreign nationals, expatriates, first-time buyers, landlords, off-shore companies, trusts, and individuals with adverse credit.

What Purposes Can Octane Capital’s Bridging Loans Serve?

These loans can serve various purposes, including quickly securing property purchases, funding refurbishments, raising capital, or refinancing existing loans. They are also useful for developers seeking planning permission, non-mainstream borrowers including foreign nationals and expatriates, and borrowers needing to complete purchases urgently such as auction and new-build purchases.

How Are Octane Capital’s Bridging Loan Applications Structured?

Each loan application at Octane Capital is structured on a highly bespoke basis and priced according to risk. The areas they lend across include residential and commercial bridging, bridge-to-let and bridge-to-sell, and they offer heavy and light refurbishment and development finance from the third quarter of the year.

Are There Any Specific Pre-planning Bridging Loan Options Available?

Yes, for developers buying property and seeking planning permission, Octane Capital offers pre-planning bridging loans. Once the planning permission is in place, refurbishment funding can be provided to cover the cost of works.